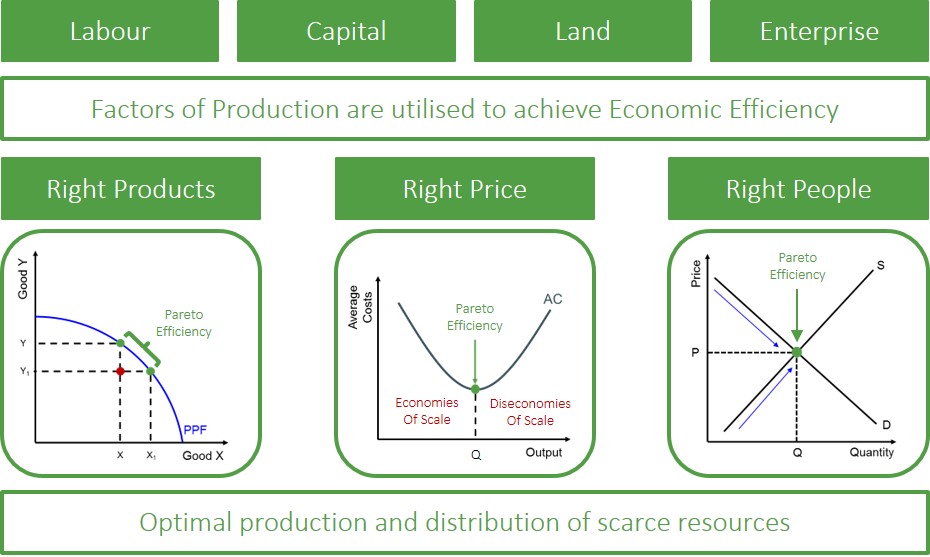

The extent to which markets produce the right goods (the combination of goods will be determined by the position on the PPF), in the right way (goods will be produced at lowest possible average cost) for the right people (market equilibrium output that fully reflects all costs and benefits).

Economic Efficiency can often be referred to Pareto Efficiency as this is the point where the optimal allocation/distribution of resources is i.e. there is no other outcome that can produce a better result.

When referring to economic efficiency it is concerned with how well scarce resources in the economy are being allocated in order to maximise social welfare by meeting the persistently changing needs and wants of economic agents in the economy. Typically, resources are allocated optimally if markets work well via the price mechanism.

Economic efficiency is achieved if firms within a market can achieve the following forms of efficiency:

- Productive Efficiency

- Allocative Efficiency

- Dynamic Efficiency

But there are many situations where the market mechanism fails to allocate scarce resources optimally and as a result this creates a form of market failure which leads to social welfare becoming reduced. The factors that can lead to economic inefficiency in a market are as follows:

- Lack of Competition - in markets where there are a small number of firms present means that these firms do not have the incentive to continually invest and innovate in productive and profitable projects and therefore this causes their costs to increase over time(X-inefficiency). These higher costs eventually get passed onto consumers via higher prices. This occurs in markets such as a monopoly, where the profit maximising output level lies below that of which is socially optimal as a result of the higher prices. Therefore, consumers cannot consume as much of the good as under a competitive market structure (allocative inefficiency).

- Presence of External Costs or Benefits - results in the private costs and benefits never equating the social costs and benefits through the market mechanism and this means that the quantity of goods and services produced by firms is either under-provided or over-provided. This occurs in markets where externalities are present such as demerit goods.

- Missing Markets - another situation where the optimal allocation of resources is not met because of the lack of provision of these types of goods from private firms. Often it is the government's role to provide this type of good to the market, but often it ends up under-consumed because of the lack of acknowledgement towards the social benefits of consuming this type of good. Examples of this are public goods and merit goods.

- Information Failure - efficient markets contain a consistent level of information across all firms and consumers and it is this that allows firms to provide the socially optimal amount of goods.

- Factor Immobility - if factors are immobile (geographical and occupational immobility of labour) it makes it difficult to firms to achieve the socially desirable allocation of resources they might not be able to allocate enough factors required to each market.