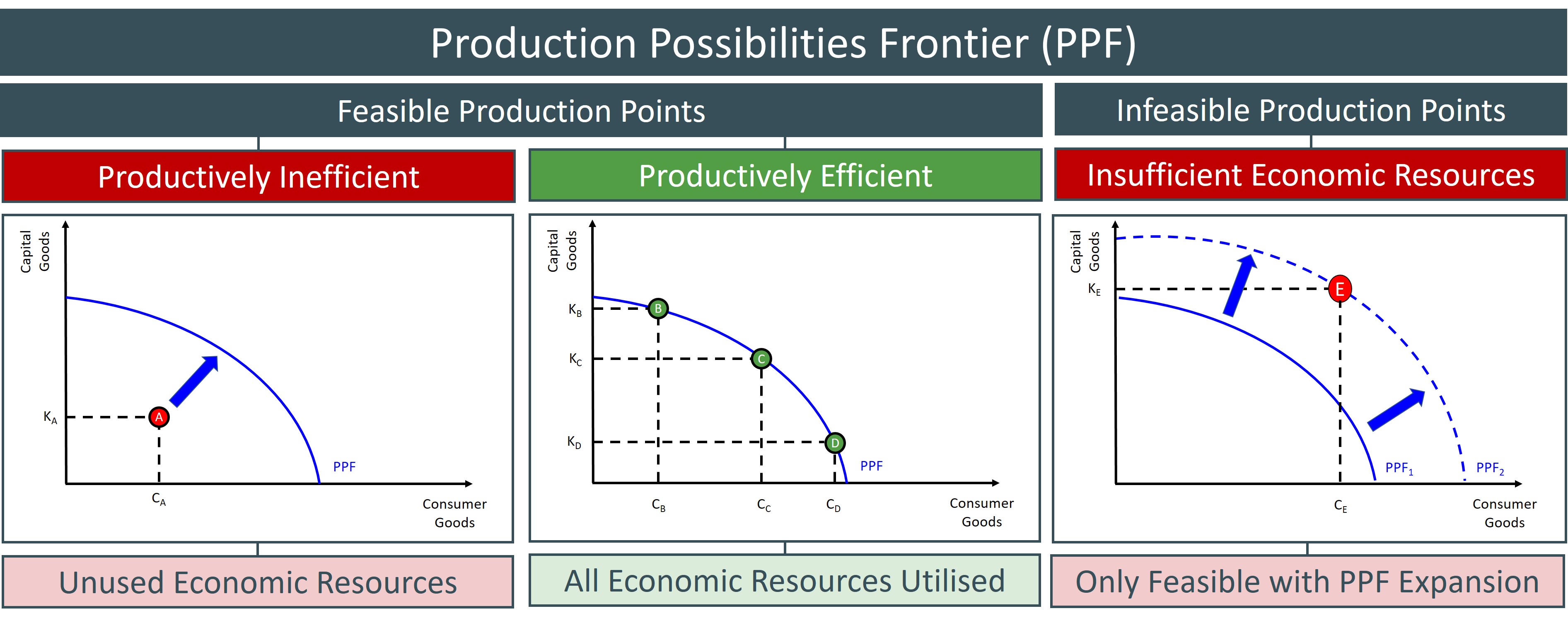

A convex curve that graphically represents the production points for an economy where all resources are fully engaged in the production of an economy's goods and services.

The PPF is the diagram that is best used to highlight the economic problem because if an economy moves from one point on the PPF to another it involves an opportunity cost as finite and scarce resources have to be diverted from one industry to another. This increases the production of one good but decreases the production of the other. The decrease in production represents the opportunity cost and this is quantified by the gradient of the PPF at any one point.

The diagram below shows the basic shape of a country's PPF, illustrating the distribution and allocation of resources towards producing goods to help the economy achieve the full employment level of output. Any point on the PPF is a point that is Pareto optimal, productively and allocatively efficient due to the utilisation of all the factors of prodcution in the economy (Point B, C, and D). However, if the economy is producing at a point inside the PPF (Point A) this represents a feasible production point, but one that is productively inefficient. This is because at this point an economy can increase the production of one good without a resultant fall in the production of another good, due to the fact that there are unemployed resources at this production point.

An economy can produce at any point on or inside the PPF. However, if the economy tries to produce at a point beyond its existing PPF (Point E), this is an infeasible production point assuming ceteris paribus. This is because even if an economy utilises all of the economic resources available any point beyond the PPF is unattainable unless an economy experiences an increase in the quality and/or quantity of factors of production available.